European Equities Decline to Two-Week Low Amid Escalating Geopolitical Tensions in the Middle East

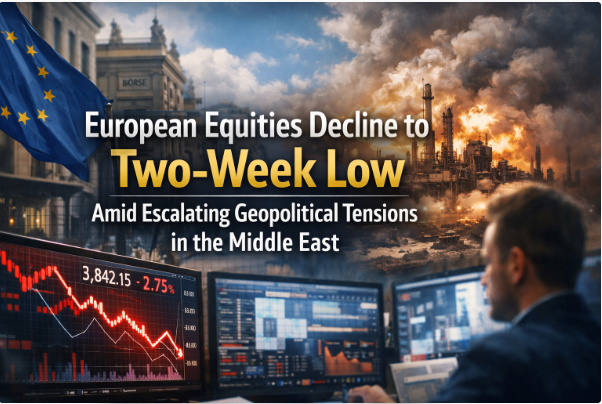

European equities started the week in a distinctly “risk-off” mood, with investors yanking the steering wheel away from optimism and toward caution as headlines from the Middle East intensified. By early trading on Monday, 2 March 2026, the pan-European STOXX 600 slid 1.5% to 623.98, marking its lowest level since mid-February and setting it up for its worst day in more than seven months. (Global Banking & Finance Review)

That kind of broad drop doesn’t happen because one company missed earnings by a whisker. This was the market doing what it always does when geopolitical risk spikes: repricing uncertainty, fast. Traders don’t need to know every detail of the endgame to know that disruption is expensive—especially when it threatens energy flows, shipping lanes, air routes, and business confidence all at once.

The bigger picture: why European stocks react so sharply to Middle East shocks

Europe is uniquely sensitive to geopolitical tremors that ripple through energy markets and global trade corridors. Even when the epicenter of conflict is outside the continent, Europe’s market structure (global exporters, multinational industrials, major banks, travel giants, luxury demand exposure) makes it an efficient “receiver” of global fear. When uncertainty rises, investors often rotate out of cyclical areas—think banks, travel & leisure, retail, and other growth-linked sectors—and into perceived beneficiaries or defensives.

On 2 March, that sector rotation was loud. The selloff was not a tidy, polite reshuffle. It was a stampede away from the parts of the market that depend on calm skies, predictable shipping, stable oil prices, and confident consumers.

What the tape said: sectors and stocks that took the hardest hits

The most immediate casualties were the industries where geopolitics punches the balance sheet directly.

Travel and airlines got hammered, pressured by route suspensions and airspace uncertainty across a region that functions as a crucial aviation corridor. Reuters reporting noted that airlines and travel stocks fell to their weakest level since mid-November, with the sector tracking its biggest daily loss since April. Major names were sharply lower: Lufthansa fell as much as 11%, while IAG (British Airways owner) and Air France-KLM dropped around 5% and 7% respectively. (Global Banking & Finance Review)

This wasn’t just market drama—it reflected operational reality. Regional disruptions were already causing widespread delays and suspensions, with carriers rerouting to avoid affected airspace and temporarily halting flights to multiple destinations. (euronews) The financial logic is simple: longer routes mean higher fuel burn, more crew costs, more schedule chaos, and weaker near-term demand.

Consumer-facing and discretionary stocks also felt the weight. European luxury—often treated like a high-beta proxy for global wealth confidence—slid, with LVMH and Kering down about 4%, while the broader retail sector declined as well. (Global Banking & Finance Review) When geopolitical risk climbs, markets tend to price in softer discretionary spending (and not just in Europe—globally).

Banks were hit too, consistent with a classic “risk-off” playbook: when uncertainty rises, markets often anticipate slower growth, choppier capital markets activity, and higher credit risk. (Banks can also be sensitive to sudden moves in bond yields and expectations for central bank policy.) Reuters’ summary of the day highlighted banks as one of the pressured areas alongside travel. (Global Banking & Finance Review)

Zooming out to the national benchmarks, the damage wasn’t isolated. Germany slid to an over three-week low; France dipped to a near two-week low; Spain hit its weakest level in more than two weeks. (Global Banking & Finance Review) In other words: this was broad-based European stock market weakness, not one country’s problem.

The “winners” in a risk event: energy, defense, and shipping

Whenever markets get spooked, the weird truth is that some sectors can benefit—not because the world is nicer, but because the economic incentives shift.

Energy stocks strengthened as oil prices surged on fears of disruption to supply routes and shipping lanes—particularly around strategic chokepoints. Separate Reuters reporting described shipping disruption in the Strait of Hormuz and noted oil’s sharp jump (reported around 9% in that account), while also emphasizing that the Strait carries over 20% of global oil shipments—a statistic that explains why traders panic first and ask questions later. (Reuters)

On the same day, other market coverage described oil spiking as much as 13%, underscoring how violent the intraday moves were as traders processed uncertainty. (Moneycontrol) That range—roughly high single digits to low double digits—captures the core reality: energy markets were pricing a risk premium, fast.

Defense stocks also caught a bid. Reuters’ market report noted gains in BAE Systems, Rheinmetall, and Leonardo (up roughly 2% to 6%), with defense sector performance supported by expectations of higher defense spending when geopolitical tensions escalate. (Global Banking & Finance Review) (Defense stocks are often treated as a “geopolitical hedge” by investors—controversial ethically, but very real in market behavior.)

Then there’s shipping—an underappreciated barometer of global stress. If routes through Hormuz and/or the broader region face disruption, vessels reroute, transit times increase, insurance costs rise, and freight capacity tightens. Reuters noted Maersk and Hapag-Lloyd up about 4.5% amid expectations that turmoil could snarl major routes and lift freight rates. (Global Banking & Finance Review)

So the story of the day wasn’t simply “stocks down.” It was “growth confidence down, disruption risk up,” expressed through sector performance.

Volatility wakes up: the market’s fear gauge starts yelling

When uncertainty rises, volatility usually follows. Reuters reported that Europe’s volatility gauge (often referenced via the STOXX volatility index) spiked to its highest level since mid-November. (Global Banking & Finance Review)

Volatility isn’t mystical. It’s the price of insurance. When investors feel they might be wrong-footed by sudden headlines, they pay more for options protection. Rising volatility tends to tighten financial conditions on its own: it makes risk assets harder to hold, encourages de-risking, and can amplify moves in both directions.

Why this matters beyond the daily close: macro data, inflation, and the ECB backdrop

The timing of this selloff matters. It hit as markets were already navigating a complicated stew: questions about AI-driven capex cycles, global tariff chatter, and persistent geopolitical uncertainty. (Global Banking & Finance Review) Europe also faces a heavy macro calendar—key inflation prints, consumer and producer prices, unemployment, PMI surveys, and retail sales—all of which shape expectations for the European Central Bank (ECB) and broader Eurozone growth. (Global Banking & Finance Review)

Here’s the tricky interaction: geopolitics can push growth expectations down while pushing energy-driven inflation pressures up. That’s an uncomfortable combination because it complicates monetary policy. Central banks prefer clear signals; geopolitics produces noisy ones.

PMI surveys cited in the same Reuters coverage suggested manufacturing in France and Italy expanding in February, with Germany showing recovery signs. (Global Banking & Finance Review) That kind of tentative improvement is exactly what markets don’t want disrupted by an external shock—especially one that threatens energy costs and global trade.

The real transmission channels: oil, rates, credit, and confidence

If you want the “mechanics” of how Middle East escalation transmits into European equities, four channels dominate:

1) Energy costs and profit margins.

Higher oil prices can benefit energy producers, but they act like a tax on consumers and many businesses. Airlines, logistics, chemicals, and industrials feel it quickly. If oil spikes, analysts start trimming margins and earnings estimates, especially for fuel-sensitive sectors.

2) Trade routes and supply chains.

Shipping disruptions don’t just delay goods—they change pricing, inventory strategy, and working capital needs. Companies with just-in-time supply models get nervous; investors get nervous about them.

3) Risk appetite and financial conditions.

Higher volatility and “flight-to-safety” behavior can tighten conditions: credit spreads can widen, equity risk premia rise, and investors demand more return to hold risky assets. That pushes valuations down.

4) Consumer and business sentiment.

Luxury and discretionary selling on 2 March is a good example. When people feel the world is unstable, big-ticket confidence wobbles—even if their personal income didn’t change overnight.

What to watch next: signposts investors obsess over

Markets don’t ask for certainty—they ask for direction. Over the coming sessions, investors will likely track:

Oil price stability: whether crude holds its risk premium or mean-reverts as clarity improves. Reuters noted EU policymakers did not expect an immediate threat to the EU’s oil supply security, but also flagged ongoing uncertainty around flows through Hormuz. (Reuters)

Air travel normalization: whether major carriers extend suspensions or resume routes. Aviation disruption reporting described multiple suspensions and rerouting across the region, which has knock-on effects for European travel demand and airline costs. (euronews)

Volatility levels: whether the spike fades (suggesting fear is easing) or persists (suggesting positioning remains defensive). (Global Banking & Finance Review)

European macro data: inflation and PMI follow-through will shape the market’s view of ECB flexibility. (Global Banking & Finance Review)

Sector leadership: whether energy/defense/shipping continue to outperform or whether the market rotates back into cyclicals.

A grounded investing mindset for messy days (not hype, not doom)

Days like this tempt people into dramatic narratives: “Everything is collapsing!” or “This is the bottom, back up the truck!” Reality is usually less cinematic and more statistical.

Geopolitical risk is notoriously hard to trade because headlines can reverse faster than portfolios can. A sane approach is to focus on process: understand your exposure, avoid leverage-driven panic, diversify across factors (not just tickers), and remember that the European stock market often moves in waves—risk-on and risk-off—while long-term outcomes depend on earnings power, productivity, and policy.

And yes, it’s okay to admit uncertainty. Markets do that every day—just with numbers instead of feelings.

Closing thought: Europe at the intersection of global capital and global fragility

The decline to a two-week low in European equities on 02-03-2026 wasn’t merely a bad Monday. It was the market reminding everyone that finance is glued to the real world, and the real world contains chokepoints—geographic, political, and psychological. When those chokepoints look threatened, capital moves.

Today’s action—STOXX 600 down, airlines hit, oil surging, defense and shipping bid, volatility jumping—is the classic signature of a market rapidly repricing uncertainty. (Global Banking & Finance Review)

SEO keyword paragraph (use as-is): European equities, European stock market, STOXX 600, Euro Stoxx, DAX, CAC 40, FTSE 100, European shares, two-week low, market volatility, STOXX volatility index, geopolitical tensions, Middle East conflict, Iran Israel crisis, Strait of Hormuz, oil price surge, energy stocks, defense stocks, shipping stocks, travel and leisure stocks, airline stocks, banking sector, risk-off sentiment, safe haven assets, Eurozone inflation, PMI data, ECB outlook, portfolio diversification, global markets, stock market news Europe, investing in European stocks, market selloff, European market analysis.